The Prescription for the Low-Income Worker

Optimal v. A Simple Budget

Everybody has a baseline financial plan, including Mike Holt, a groundskeeper in Marina, California. Mike’s financial trajectory is dictated by his income and is instructive for how planning should be executed for lower-income households. The usual tack of financial writers toward lower-income populations always misses the boat. Mostly, advice is a rehash of spending less, paying credit card debt, and getting a budget. Impersonal, meaningless, and intellectually indefensible.

Often, we think sophisticated, “I am willing to pay for it,” planning is for the mid to upper wealthy. It is not. If the approach is principled and intellectually grounded, then planning can be relied on wherever the household rests on the wealth spectrum. Once household investable wealth is more than $10 million, planning requires more money for protective and estate transfer reasons, but even then, a PWM would add value to their client experience with a baseline financial plan. Suppose you are a $50 million reader. Would you like to know your expected living standard for the year, the measure of how it is at risk given the variance within your advisor’s investment suggestions, and how tweaks to your planning today affect your expected living standard tomorrow? In a subsequent post, I will follow up with the baseline financial plan for a relatively wealthy, retired couple. Not Silicon Valley, hit an IPO home run wealth, but upper middle class.

Mike’s Baseline Plan

There are about five hundred benefits of the baseline plan; the top one is the small amount of information needed for initial plan development. The list is in this post, and for a single like Mike, the list is truncated. Mike is 22, earns $43,000 with an employer that contributes to Mike’s 401(k), lives in an apartment that costs $2,150 per month, including utilities and insurance, and resides in California. No credit card debt and $1,200 today in a bank checking account. Straightforward.

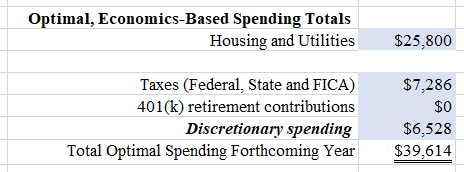

Under the hood, a lot is going on: Inflation and investment expectations, Mike’s prospective Social Security benefits, and Mike’s prospective income taxes, all cuddled by a dynamic programming algorithm. Commercial software handles all of that. Mike’s baseline sustainable living standard is $6,528 for this year, indicating his maximum spending beyond his cost of housing, expected utility costs, and taxes, a little more than $500 per month. That is advisory done well for Mike, and whether he wants to be diligent in tracking his actual monthly spending toward this target is his choice. A budgeting app, or occasional arithmetic, comes at the end of the planning to execute the plan if Mike wants to track the attainment of his target. Others may be interested in planning but want a third party to hold their feet to the fire.

For non-profits and pro bono planners interested in fertilizing financial awareness among the low-income population, their process should start by determining the best spend and then facilitate monthly follow-up to promote the prescribed financial behavior.

The principled approach to baseline financial planning will reveal specific recommendations sensitive to the household. Recommendations will vary because each household has its magic number. Some low-income households may not have to cut spending in response to achieving their optimal living standard. Low-income households are not, de facto, spendthrift households. Rules of thumb rarely hold. The best course of action for the first year of a baseline financial plan will always be informed by the optimal living standard estimate and comparing prior period actual expenditures, revealing the best course of action.

How Should Mike Respond?

Let’s return to Mike. Given his baseline plan, he may have no interest in the baseline outcome, satisfied with how he spends to enjoy life. Or, he may be willing to dig deeper to ensure he is living his best financial life. Can he spend more? Should he save more? With Mike’s optimal spending in tow, gathering Mike’s actual spending is the next step.

Most of us, when asked to identify how we spent money last month, will omit two or three significant cash outflows: taxes, retirement contributions, and pre-committed, automated savings for an emergency fund or a planned special purchase. What is the breakdown of Mike’s most recent annualized actual spending? Below is a listing by broad budget category, and only taxes of $7,286 must be added back to get Mike’s complete spending picture. Mike’s spending list extends housing and utilities by other ways he likes, some non-discretionary like food, and others by his lifestyle choice.

Mike’s actual spending is $47,306 when adding taxes, higher than his $43,000 pre-tax income and substantially above the optimal target of $39,614. Add taxes he cannot avoid, and his current living standard is unsustainable. Cutting from the list of actual expenses above, Mike needs to lower spending by about $7,700. If Mike reaches his optimal spending target, which is well below his current income, there is a savings prescription, too. Income less optimal spending equals savings of $3,386. Why does optimal planning require Mike to save? Savings are driven partly by Mike’s plan to retire at age 67 with the expectation of living to age 90. (Both were known when solving for today’s optimal plan.) Twenty-three years of retirement needs to be funded privately along with Social Security retirement benefits. Thus, the savings prescription works hand in glove with the spending prescription to support the living standard for Mike, which is achievable each year for the balance of his life.

Savings to support a sustainable living standard is unique to economics-based financial planning.

Mike’s Next Steps

Mike is not in an unsurmountable pickle because he has his human capital and ability to derive an income. And he has numerous choices about how to cut near-term expenses. Mike can work in a state with no income tax and lower price per square-foot rent charges. Mike could take on a roommate and, like Jorge Cortez, get the advantages of shared living. Mike could stay in his apartment, cut his auto expenses, restaurant spending, and “fun” shopping. If Mike worked with an advisor, the advisor could present 401(k) investment scenarios with slightly higher return/risk profiles that may permit Mike to save less for retirement and transfer the funds to current spending. Financial planning strategies are innumerable, regardless of a household’s financial prospects.

Mike isn't in a good position, and the answer isn't for him to save more. He's paid too little. I'm not familiar with the cost of living where he is -- my mortgage payment is less than half of what he pays for rent, because central Illinois is a different world. I'm willing to concede he may not be able to find a cheaper place to live in his area (although I'd definitely try to get a roommate. Easier said than done to find a reliable person, though.)

Even so, it's also true that his wages are higher than what I made running a newsroom less than a decade ago. So even if he were to move to a place with a lower cost of living, that won't help him because his pay will be slashed to about half as much.

Even if he eats from dumpsters so he can stop buying food, the little bit he can save isn't going to be enough to allow him to invest anything meaningful for his retirement.

He's not in a good position. He's not going to be able to pay for his retirement unless something changes quite dramatically.

To tell someone whose entertainment budget for the year is $180 that he needs to cut spending is, quite frankly, cruel.

What’s missing from this is medical costs. His income in CA (where I live) would make him eligible for Medi-Cal. If that’s how he’s obtaining medical care, good for him. If not, then he should apply.

He’s young and healthy…for now. One accident could change that. As he grows older, what’s the plan for medical costs?