Jorge Cortez and the Dallas Cowboys

The Benefits of Shared Living

Jorge Cortez is a guy working hard and choosing to enjoy life. Single, Jorge works for a moving company, and the love of his life is the fall NFL season. A hard worker but employed at relatively low pay, Jorge’s passion is the Dallas Cowboys. Every home game, he treks to Arlington for a full day of tailgating, opponent taunting, and an embrace of the expense. Jorge spends a lot of money on Sunday. His meter of fun is pushed so high when attending games at AT&T stadium he had to move his church going to Saturday for the last four months of the year. No matter if he is lining the Jones family’s pockets, it is worth it to him. Some might think, “Wow, how can he afford it?” “Is that a good idea?” How do you judge Jorge’s spending? If you meet Jorge, it will take about a nanosecond to get caught up in his thrill. It is infectious.

There is a personal finance lesson underneath the preferences of Jorge Cortez centered on how he values money. Nobody else can judge Jorge’s spending life better than Jorge. My choices do not matter. A talking head’s judgment does not matter. Dave Ramsey yelling, “Spend less, Jorge!” does not matter. Too often, opinions about the finances of young adults and lower-income workers are not generous. Usually, they are offered based on a moment in time outside the context of a more extended period. Viewing Jorge as an income-producing machine, the last thing he needs to do is tamp down his pro sports spending. Jorge’s psychic benefit loss would be enormous, and it would be painful to see his disappointment. Non-economic financial recommendations based on rules of thumb can be damaging.

General advice to “Spend less, and start saving!” can be just plain wrong and unhelpful.

Today’s food for thought may explain Jorge’s preferences for spending are well aligned with any third party’s assessment of his finances. Jorge’s counter-example is that he is taking advantage of the benefits of shared living. Beyond the Cowboys, his cost of living is low, and his standard of living is higher because many of Jorge’s non-discretionary expenses are shared.

Shared Living

There is an intuitive and measurable living standard effect of shared living distinct from living alone.

The intuition:

Cohabitation has benefits because primary, non-discretionary expenses are at least halved. A rent or mortgage payment that puts a roof over a single person’s head, typically about 30% of pre-tax income, is no different when two or six people live in the same space. On a per capita basis, the cost becomes lower incrementally. Throw in the splitting of property insurance, household internet service, streaming TV, and a lower per-person utility bill, and the expectation of shared living benefits is clear. The longer-term effect can be dramatic. Shared living can be the difference between Jorge’s NFL indulgence or a Sunday afternoon at home alone, watching the ‘Boys from the couch and popping tabs on a few Buds.

The measurable:

Boston University economist Laurence Kotlikoff measures the benefits of shared living this way. If a single adult with annual discretionary spending of $20,000 this year adopts shared living, discretionary spending would increase 25%. Essentially, two adults living together can live as cheaply as 1.6 adults living alone. The benefits of shared living are moderated once the two adults introduce a child. The normalized adult living standard goes down, in the range of 20 - 30% with the first child. The effect of a second, third, fourth, etc., lowers the household adult’s living standard but at a declining rate. However, good economics are coming for child-rearing adults because of aging. Parents feel the bonus effect when children move out and on their own—their living standard increases.

Because adult living standards benefit from shared living, there are other applications for household economics.

Divorce settlements and life insurance purchase recommendations are driven by the same shared living principles.

Take the tragedy of premature death. A household clicks along at a living standard tied to the adults' incomes, and then one dies. If the deceased were the substantially larger income producer, it would be impossible for the survivor to replicate the living standard to which they have grown accustomed. Proper planning using shared living principles will nail down the appropriate amount of life insurance to buy. I illustrated this problem and its solution with the Madigans, a couple in south Florida.1

Jorge’s Measurable Living Standard

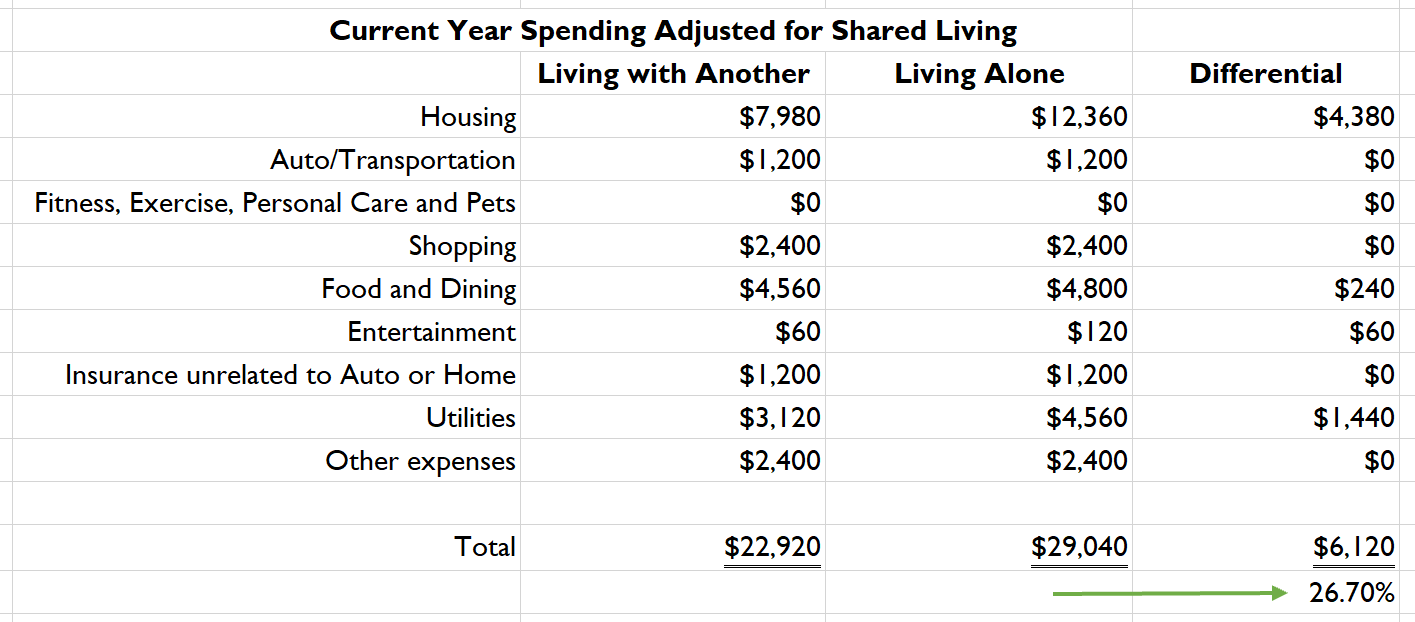

How is shared living working out for Jorge? Specifics matter, and the question centers on which of his typical expenses would be affected if he moved from sharing with a roommate to an apartment of his own. Jorge’s two-bedroom apartment costs about 20% more than a one-bedroom, but moving solo to a one-bedroom means no more fifty-fifty sharing of the rent. Also, Jorge has sharing economies for utilities and food staples that would be lost if he lived alone. The differential between shared living and living alone would be a 26.7% increase in Jorge’s living expenses.

Whether the differential is consequential depends on Jorge’s after-tax income. Jorge makes $30,000 a year gross and nets about $26,000 after federal tax and social security employment taxes under current tax rules. Jorge’s total cost for a Cowboy’s game is $300, beginning with a $50 standing-room-only ticket: $2,400 or a little under 10% of after-tax income for this year’s eight-game home season. Shared living keeps Jorge’s spending at about break-even relative to income and within his means.

Jorge should continue to live his life his way. That, too, is a tenet of sound financial planning.

Complete archives of articles are available to all paid subscribers. If you are a free subscriber and want to read any article, send us a note, and we will get it to you: team@finplanllc.net.

In my opinion, financial decisions are not a one-size-fits-all scenario. Spending choices are essential to ensure you are still financially safe for necessary items. This mainly relates to low-income workers or young adults. Jorge Cortez likes spending money on Cowboys games, and there is nothing wrong with that, but in order for him to do so, he has to save money in other areas of his spending. We see in this article that Jorge lives in a shared living space. Shared living is a great way to improve one’s living standard without increasing discretionary spending. This effective living strategy allows Jorge to save enough money to continue spending money on the Dallas Cowboys without straining his budget. It is important that individuals make financial decisions that align with their values and passions, and this is precisely why Jorge spends his money on Cowboys games.

For Jorge, shared living allows for his standard way of living. Even though many may not agree with his spending habits, Jorge can still manage a standard of living while partaking in Dallas Cowboy's festivities. As mentioned in the article, living alone would be a 26.7% increase in Jorge’s living expenses. However, one thing to consider is the future. Does Jorge see himself getting married or having a family? What if his roommate decides to leave and now all the rent is placed on Jorge’s shoulders? If there are any concerns would Jorge consider just tailgating at the stadium and not getting a ticket or going on special occasions? For many, shared living is appealing because it lowers expenses, company is always provided along with still having personal space. Each person is subject to their own spending habits and what areas they wish to spend more money, for Jorge, he is able to afford non-discretionary expenses while splurging on the Cowboys.