Low Income Households

Answering the retirement question

How do you tell a lower-income household they need to save for retirement?

The members try to stay afloat, eat, and pay the basic bills. Next week is prime time for them, not forty years from now.

There are good reasons to expect people to plan for retirement. One is that there is little chance retirement will be avoided because of the physical skills required to do the job. Roofing labor working in the summer heat in Georgia is one. Landscapers like Mike Holt, who isn’t much interested at age 70 in toting rock and soil and climbing up a tree to cut a broken limb, is another group.

What should be the retirement plan for those who need one and reside on the lower end of the annual income scale? Two benefits inform the financial prescription.

Planning for retirement may have explicit tax benefits

Social Security retirement benefits are available at age 621

Mike’s Retirement Plan

Mike Holt lives in northern California, earning $43,000 gross this year.2 Single, without the financial benefit of a shared living or a spouse with an income. Absorb Mike’s monthly expenses, which are annualized in the table below. $40,020 before any consideration of income and payroll taxes.

Do Mike’s expenses reveal a problem?

There may or may not be one.

A rich Uncle could supplement Mike’s income. Mike may have a bank checking and savings account. Even an individual retirement account. Financial assets are not a part of the monthly spend.

To add some color to Mike’s financial picture, there is good news and bad news. Mike has no unpaid credit card debt, but his only financial asset is a $1,200 checking account. He has no other savings or individual retirement accounts.

Mike’s Prescription

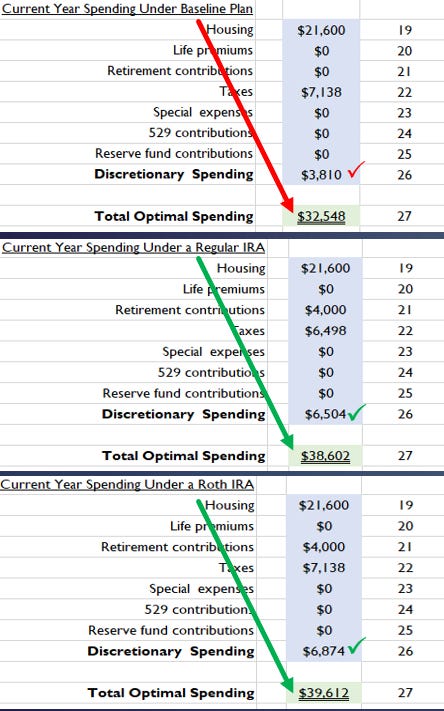

At Mike’s income level, he would need to cut his spending if he wanted a sustainable living standard path that permitted him to retire at age 62. If you add back Mike’s federal, state, and payroll taxes ($7,138) to his current budget, his actual spending is $47,158. His economics-based baseline financial plan (the top chart with the red arrow) requires a spending cap of $32,548 next year. That would guarantee he is saving $10,453 ($43,000 income - $32,548 total expenses) toward his retirement to begin at age 62. But for the current year, he has to figure out how to live on $3,810 after housing and taxes. An impossibility. His utility bill alone is higher.

Two other savings alternatives exist for Mike. A regular IRA and a Roth IRA, differentiated by tax benefits while permitting the same types of investments as the baseline plan.

The middle table lists recommended current year spending when a regular IRA is used for retirement, where Mike deducts contributions to the IRA. Mike explicitly adds a $4,000 annual IRA contribution up front and is restricted to $38,602 of total spending this year. The spending he has available this year, above housing, his $4,000 IRA contribution, and taxes, is $2,694 higher than the baseline plan, but obviously, he still needs to cut. Over the long run, using the IRA choice to help fund his retirement living standard is valuable. It increases his lifetime discretionary spending by $211,474 above the baseline plan.3

Conclusion: regular IRA at the $4,000 funding level is better than baseline in the long run.

The bottom table lists recommended current year spending when a Roth IRA is funded with $4,000 and used for retirement. The Roth contribution isn’t tax-deductible, and Mike’s current tax year does not change. However, Roth account values increase tax-free, and withdrawals are tax-free. The result for Mike is that a Roth gives him slightly more spending power for the current year than a regular IRA, $370, and over a lifetime $25,586 more discretionary spending in today’s dollars.

Conclusion: A Roth is slightly better for Mike than a regular IRA over the long run.

What Should Mike Do?

Funding a sustainable retirement appears bleak because there is too much to give up to live today. Mike has flexibility and trade-offs to consider. I have recommendations to give him a higher living standard that I will share after I read your thoughts.

What would you recommend?

More savings into a regular IRA or Roth?

Should Mike Move?

Comments are open to everyone.

This social benefit is available in the U.S. and age 62 is the first age benefits can be withdrawn. Depending on health and longevity, waiting to withdraw may be financially preferred because of actuarial adjustments to monthly benefits that begin at older ages.

This result is in the complete financial plan and is free to paid subscribers upon request.

The members try to stay afloat, eat, and pay the basic bills. Next week is prime time for them, not forty years from now. I read this and it got my heart going faster.

I used to work in a finance office of a nonprofit with a lot of employees in a less well off part of town. Only the top executives took advantage of the 403b match. I looked into it, and boy this article stopped me. This message is just a tough thing to teach and encourage when people are in this range. It did show me how the "match" concept wasn't so great for lower income people.

I used to work 80 hours a week at a desk job. Outdoor work wouldn't be possible for this schedule, but maybe somehow find a less strenuous job and work a lot more hours. (with healthcare hopefully)