Savings Lessons for Retirement

Day 26. Follow these principles to determine whether a Roth or regular IRA is better

Readers, I am at the end of my semester with my undergraduate students, many of whom are on their path to a new job in the near future. Some will be able to participate in an employer-sponsored 401(k) plan. In that event, there will be mutual fund choices to make and get right.

Others may want to save for retirement, and there are better choices than plugging a few dollars of after-tax income into a bank savings account. Many will think, “Retirement, you must be kidding? I have a life to live.” True enough. A new job affords a higher near-term living standard today. Still, if there is an iota of preference for retirement, then the amount of savings that balances the best financial life across an expected lifetime is a number to be calculated. Yes, it is determined by household economics, not a rule of thumb.

Last week, I closed my life-cycle economics class with a proposition for my students:

If a household wants to save for retirement, is saving through an Individual Retirement Account or a Roth IRA the better choice?

The answer can mean thousands of dollars for you, too.

You may have an IRA, want to keep it, and try a Roth next year. Or vice versa. There is a rational reason for having both: taxation differs. Having both accounts gives the benefit of tax diversification: retirement withdrawals from an IRA are taxed just like job-related income. Retirement withdrawals from a Roth are tax-free! The “what should I do” is dependent on your attributes. 1

Johnny Sullivan’s updated story from a prior post illustrates the measurable consequences of a retirement vehicle choice unrelated to how the money is invested. The first lesson is low-hanging fruit,

Lesson 1: The better choice produces the higher expected lifetime living standard.

Johnny Sullivan

Johnny Sullivan grew up an East Coast boy who attended Oklahoma for college. Even now, when fall sets on the southern prairie, Johnny can still smell the winter wheat, and his mind turns toward tornado season and away from the memories of the bitterly cold winters when a Nor’easter would blow through every crack in his boyhood home.

Johnny is single, which might be explained by his avocation: storm-chasing. Johnny is on his way to Kansas to start his first job out of college. He is going to work in Wichita for KU Social Media, LLC. A graduate of Oklahoma State University, Johnny was a double major in communications and earth science and a long-distance swimmer on the Cowboy swim team. Johnny grew up in Lowell, MA., and started “The Tornado Club’’ in high school. An avid follower of weather forecasting, Johnny wanted to attend college in Oklahoma and live in Tornado Alley. He fulfilled his dream.

Johnny, a curious student at OSU, graduated with a 3.45 GPA. It would have been higher, except finals were in May.

Storm-chasers can’t be concerned with the academic schedule.

In college, Johnny became interested in how social media affected people’s perceptions of a daily weather forecast. Did weather followers value social media? If so, which platforms did they prefer? How do they post? How did the platforms use posting frequency and depth to their business advantage? Who, besides Al Roker, is an important influencer? How many people put the WeatherBug on their desktop? Typical questions require some analytics. Johnny received multiple job offers, and KU Social Media offered a $10,000 signing bonus to seal the deal.

Johnny strongly prefers to begin saving for retirement. KU Social Media’s benefits package is built to attract and support a younger employee base. There is no need for an employer-sponsored 401(k) when a minor amount of health insurance, an on-site spa, and free food trucks have been voted the benefits most cherished by Social Media’s Gen-Zers.

Johnny is a saver, an uncompromising preference enforced by his upbringing among the frugal elites. Now that he has a full-time job, he wants to make his first serious effort toward saving long-term. A regular IRA and a Roth IRA are the obvious choices because they come with tax benefits. However, savings for retirement in the near term are challenged by other calls on Johnny’s income. Repaying a student loan he received in Stillwater is as much a non-discretionary expense as Johnny’s food, shelter, and clothing. His annual repayment is $3,374 per year. Yet, some savings might be workable, and Johnny devotes saving $2,000 per year to his retirement basket. Taxation differences among tax-favorable retirement accounts, investment returns, and other household financial characteristics complicate the better way to save. Johnny’s better solution is his answer to Lesson 1,

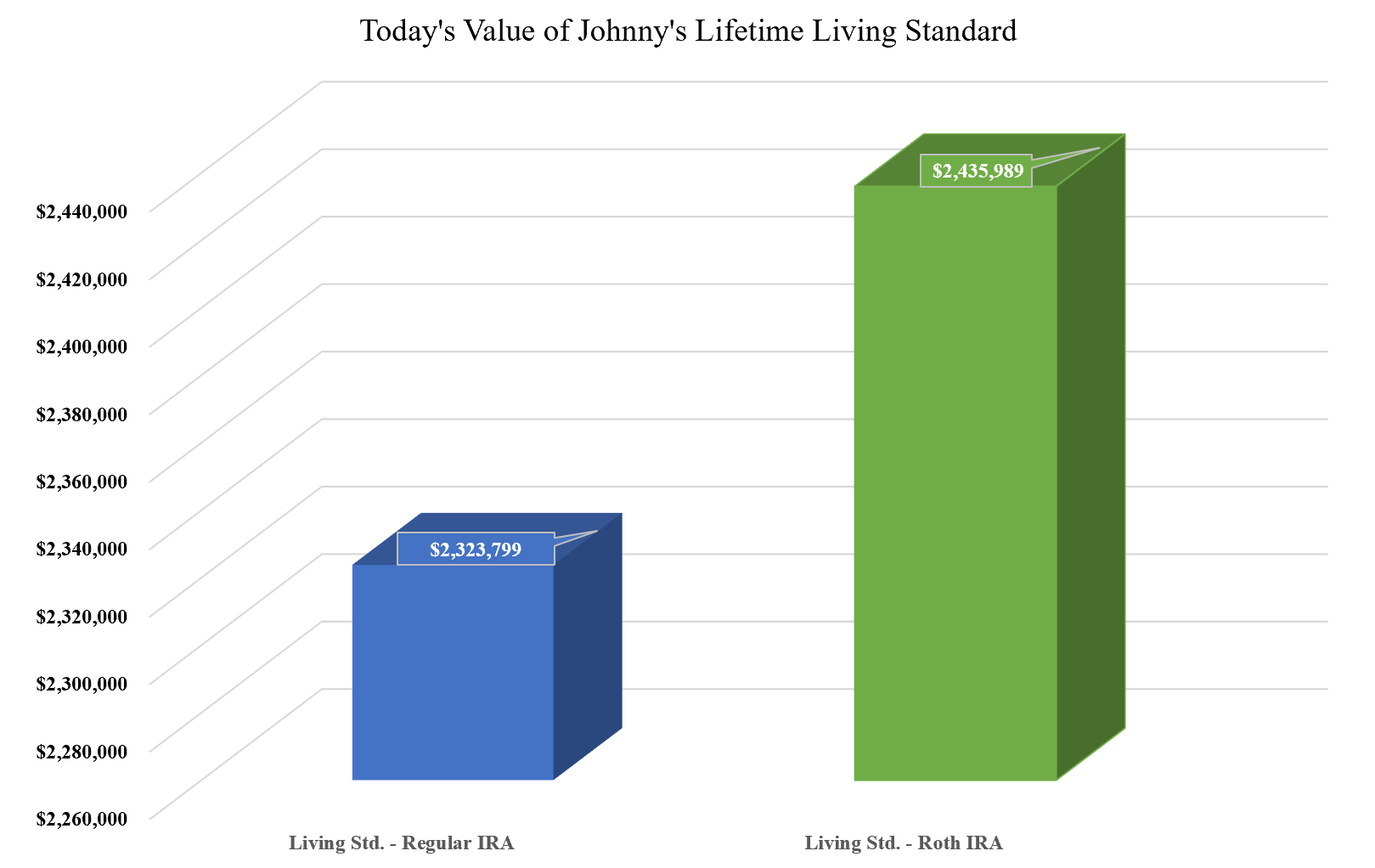

In Johnny’s case, the effect of a regular IRA and a Roth IRA yields a difference of more than $100k!

Roth or Regular IRA for You?

What would you do if you were in Johnny’s shoes and wanted to make a better choice? Like Johnny, you might search for information about IRAs and Roth IRAs. Johnny begins with the sites of three major investment companies: Fidelity, Schwab, and Vanguard. They compare and contrast the Roth and regular IRA choices on their retirement tabs. A glimpse below at the information delivered shows the standard delivery of the content.

1. Fidelity

2. Schwab

3. Vanguard

See a theme? Leading investment companies, but the information pool is shallow. Descriptive information about contribution maximums and the tax law. There is no indication about savings needs, investment choices, or the better choice because taxation is different and households are different. Wouldn’t that be valuable?

Thousands of dollars are at stake in making the better choice. How can an answer to the regular vs. Roth IRA question be more helpful for you? You can rely on me and Personal Finance Economics because banks and investment companies can't get their public presentations to the required level of detail to answer the question with the degree of seriousness everybody needs for decision-making.

Johnny Sullivan’s Better Choice

Johnny’s better choice relies on Johnny’s financial attributes. To re-emphasize, the better advice for Johnny may not be the preferred choice for another Gen-Zer or a 50-year-old couple with kids. Household financial attributes turn the decision toward the best option. The solution is generalizable and effective for households, advisors, and CFPS because it is grounded in economic theory. Readers don’t need to know a lick of the theory to apply it because the practical engine has been built, and you have me to help.

To illustrate with Johnny, consider that he will earn $78,000 this year and wants a reasonably typical working lifetime, retiring at age 70. Health and family genetics make him expect a long life to a maximum of 90. Prospectively, about 50 years of life with employment and 20 years post-employment. Living in Kansas implies a specific state income tax, and we will hold federal income taxation and social security benefits consistent with current law. Housing expenses are $2,350 per month, and whether Johnny contributes to a regular IRA or Roth, he plans on contributing $2,000 per year, adjusted for 1% growth. All other financial planning details and assumptions are listed in the financial plan, which I will share an updated version if you DM me.

Why would Johnny’s better choice require a more complete approach than describing contribution limits, deductibility rules, and tax effects on accumulations and withdrawals?

The tax law applies differently to different plan types, and the earnings on supporting investments matter.

Roth account assets grow tax-free and are withdrawn tax-free, while regular IRA account assets grow tax-deferred and are taxed as ordinary income when withdrawn.

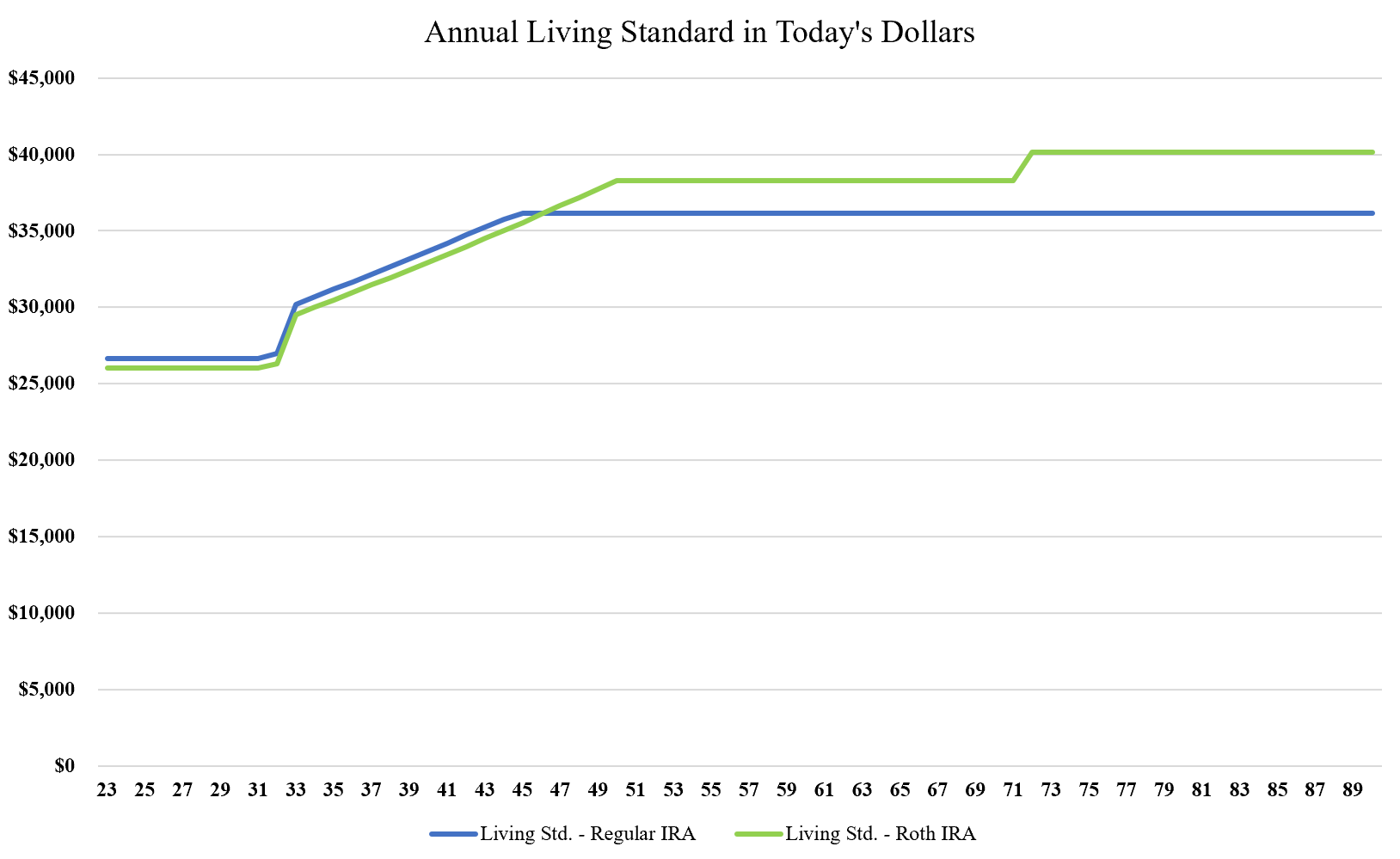

Johnny’s solution is found in the two charts below. The upper chart tracks Johnny’s living standard year-by-year in today’s dollars. Under the Roth alternative, Johnny’s living standard is generally lower until age 46, then higher every year after that. The much higher and total effect is the criterion for decision-making.

The cumulative difference in lifetime living is about $110k in favor of the Roth IRA—that is too much money to give up by making the incorrect decision.

Two reasons for this difference. First, lifetime income taxes are lower under the Roth alternative, and second, prospective Medicare Part B premiums are higher. Most of the value the Roth choice adds extends from the tax savings.

What Would Cause the Results to Change?

Generally, the higher the investment returns from year to year, the more value to a Roth. Lower investment returns take away some of the Roth tax advantages. In Johnny’s case, it was assumed that Johnny would earn about 3.75% in real terms on his retirement assets. If his returns only match inflation, with 0% real returns year-over-year, then the regular IRA becomes desirable to Johnny based on Johnny’s comparable living standard under each account type.

Lesson 2: If you are engaged in retirement planning, you have the best choice for your household: an IRA, 401k, 401k with an employer match, or a Roth.

You start with a baseline scenario as if you contributed to a regular IRA. Measure the living standard.

Run a second scenario as if you contributed to a Roth IRA. Measure the living standard of the second scenario.

Compare the two scenarios and elect the one with the highest living standard.

That is another piece of low-hanging fruit. Our book dedicates Chapter 7 to retirement.

Final note: Chapter 3 of our book explains how to run a baseline scenario for any household financial decision. For those who prefer video guidance, that is coming in January 2025.

Comments are wide open for all subscribers.

Many individuals have 401k plans through their employers, which allow higher contributions. Having a 401k and an IRA is plausible, but that would be another question to answer. Of course, the living standard approach still applies.

Will there be a video about this? You mentioned a video coming out in January. This post was very helpful as I am also a college student who is trying to learn and understand more about what these terms mean.

This is one of the things I could never figure out before I learned how to compare the difference in living standards. The article did a great job detailing it!