Your Returns Must Be Real

Your Returns Must Be Real

Tools to manage inflation risk

How is your grocery bill? Have you seen the $25 meal deal at McDonalds? Maybe Chipotle will offer a $30 burrito bowl. Inflation affects our living standards and how we should think about investing.

Economics-based Personal Finance is moving through Chapter 5, the first chapter on investments. Last week’s installment offered historical return information on four classes of assets from 1928 to 2023.1 Reported returns are annual average returns, and the table below lists returns as “nominal,” the typical way savers and investors think about returns. If your bank is offering you a savings account with a 4% annual percentage yield (APY), the 4% is the nominal return.

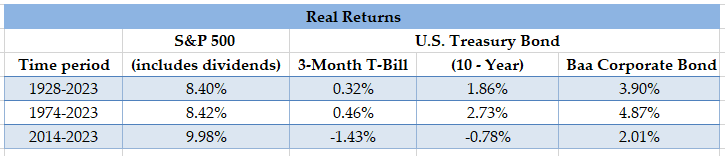

The second table reports “real” average annual returns over the same time periods for the same asset classes. They are lower, and in the case of T-bills and 10-year Treasuries, returns have been negative over the last ten years. What is going on?

Real returns consider inflation and offer a second perspective about investment returns: are my investment returns keeping up with my purchasing power?

Readers can infer that if inflation exists, salary raises and investment returns need to at least match inflation.

The installment is longer than normal, and it includes a presentation on “The Mechanics of Stock Market Investments.” How to evaluate making and losing money in stocks, investing strategies, and unreliable ideas about investing in stocks provides a prelude to next week’s installment on mutual funds and ETFs.

Today: How does Melinda Olvera manage household finances in a higher inflationary environment? If there is an extended high inflationary period, there can be severe economic discomfort. In today’s installment, I Bonds and TIPS are presented as spots for savings dollars that protect returns from inflation.

Excerpt:

Keep reading with a 7-day free trial

Subscribe to Personal Finance Economics to keep reading this post and get 7 days of free access to the full post archives.