Early 50s, single, and wants to splurge. But, be okay.

The subject of the article, Carrie Mitchum, wants to spend and maintain a sustainable living style.

This is a bread and butter financial question that life-cycle economics solves quickly.

You may not have the same question today, but if you wanted to know how much to spend and save to maintain your standard of living, you’d be ahead of 98% of the crowd.

How do A+ planners answer the “Can She Afford It” question? Consider the resources in hand, household income, interest in work, longevity and a few details.

Here is the way to think about it

Income this year — and over time?

What's in checking, savings, investments today?

Retirement accounts: Roth, IRA, 401(k)?

Social Security, taxes — under today’s rules.

Three other things: want to retire, expect to live long, and how do you feel about stock market risk?

The Results

Life-cycle economics produces the annual spending cap. How you spend within the cap is at your discretion.

The spending cap is estimated for each future year, and the savings plan is based on it. The model runs under the hood. You don’t need to know the math to make sense of the results.

Applied to the “Newly Single”

I took the information from the WSJ article for Ms. Mitchum to calculate her spending cap next year and to her max age (100). The article is very rich with financial details but obviously incomplete. I used MaxiFi Planner and made a few assumptions.

Here is some of what I know.

Ms. Mitchum lives around Washington D.C. which is relevant for taxes.

Earns $200k per year. Has a brokerage account and cash valued at $437,000.

Owns stock valued at $561,000.

Has an IRA valued at $941,000 and a 401(k) valued at $403,000.

I turned the software crank.

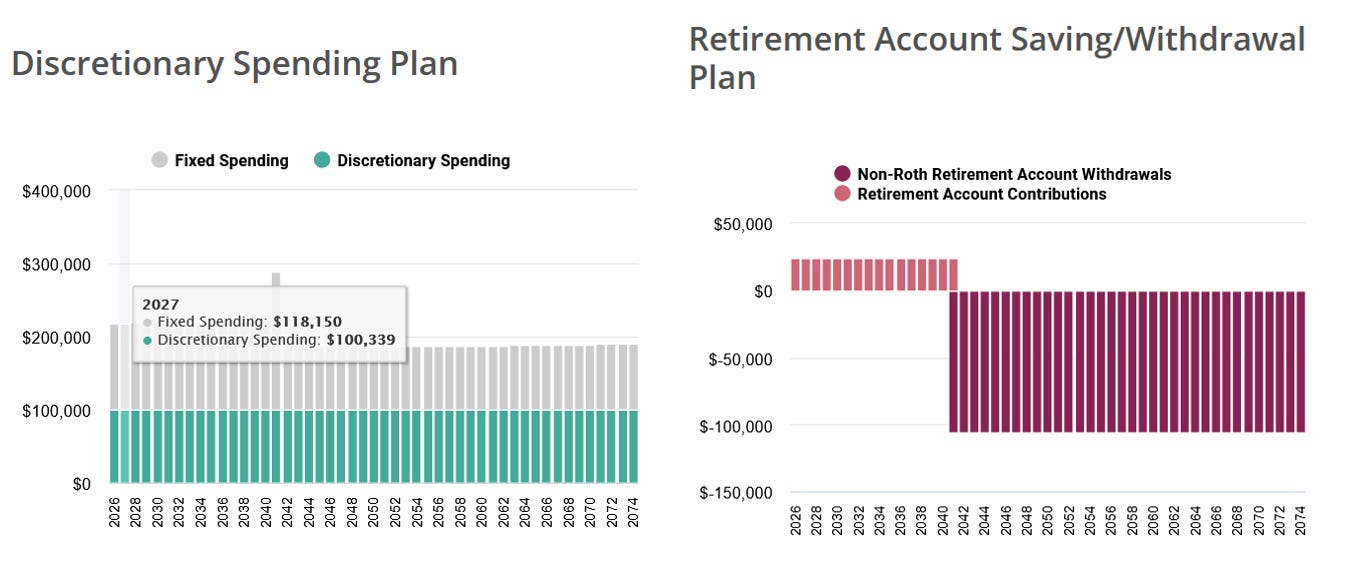

Ms. Mitchum’s spending cap in 2027 is about $218,500. $118,150 is her housing expense and taxes. The difference is her discretionary funds, $100,339, to cover everything else.

The above graphic shows Ms. Mitchum’s annual spending caps for the balance of her life and her retirement accounts. Given her optimal spending path, retirement savings and withdrawals are mapped out over the same time period.

Pretty cool. And, a sustainable path.

Her affordability question for 2027 is now guided by a specific result: $218,489.

If she moves, changes jobs, decides to retire before age 67, or the macroenvironment changes, a rerun of the plan will update the spending caps.

That is what economics-based thinking does. Provide an initial, base answer, then update annually or when life changes.

If you’d like your own “Can I afford it?” plan built with life-cycle economics with my guidance, that is a feature of being a VIP.

Questions? Message me. I read all subscriber messages.